Full Report

The numbers behind FactSet Research Systems Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ thousands unless noted.

Reading notes: Display unit is thousands of US dollars (US$ thousands), exactly as FactSet's consolidated statements are printed ('in thousands, except per share data'). Per-share and KPI-count rows are exempt from that scale. FactSet's fiscal year ends August 31. Each fiscal year is cited to its own Form 10-K (FY2021–FY2025); every value in the five annual statement columns is verified against the cited filing page. Income statement presentation drift: the FY2022, FY2023 and FY2024 10-Ks break out an 'Asset impairments' line below SG A; the FY2021 and FY2025 10-Ks (and the standardized data feed) fold it into SG A. This tab shows each year's own-10-K presentation, so 'Asset impairments' is $0 in FY2021/FY2025 and SG A for FY2023/FY2024 differs from the data feed (see discrepancies). In FY2021 and FY2022 the income statement reported interest on a net basis ('Interest expense, net'); FY2023 onward splits Interest income and Interest expense. The Interest income/Interest expense rows are therefore blank for FY2021–FY2022, while 'Total other income (expense), net' is populated for every year.

Share Price — Full Available History — 30 Years

The stock closed at $262.46 on Jul 16, 2026 — up 26,501% over the window shown (+20.4% a year), trading between $0.78 and $495.72. At that close the stock trades at 17× FY2025 diluted EPS as reported below.

Source: market price feed, monthly closes, sampled from 7,559 source observations, Jun 1996–Jul 2026. Price return only, excludes dividends. Prices are split-adjusted (×1.5 on Feb 08, 1999; 1:2 on Feb 07, 2000; ×1.5 on Feb 07, 2005).

FY2025 at a Glance

Revenue (US$ thousands)

Operating income (US$ thousands)

Net income (US$ thousands)

Diluted EPS

Source: FY2025 consolidated statements [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

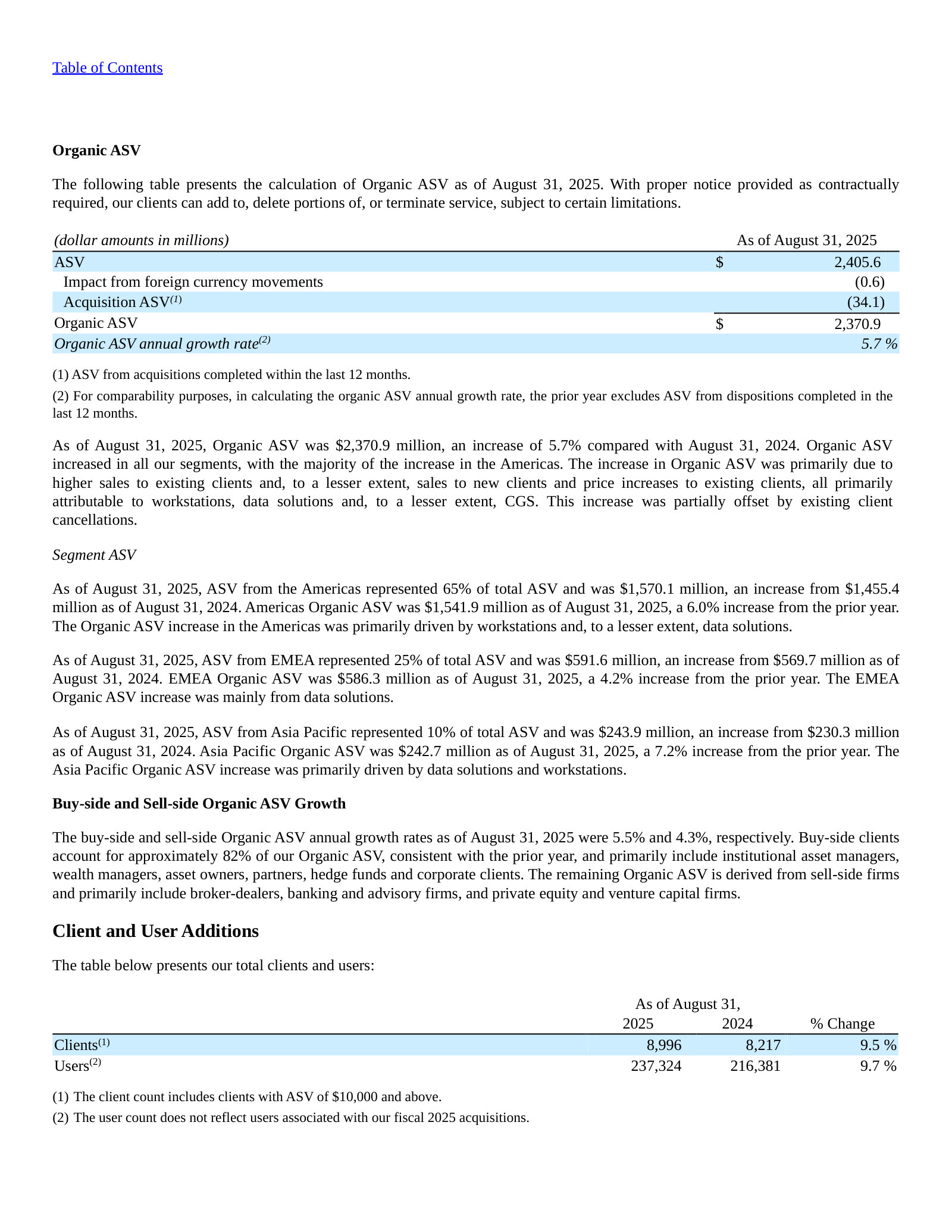

Revenue by Geographic Segment

| Revenue by Geographic Segment | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Americas | 1,008,046 | 1,173,946 | 1,335,484 | 1,419,901 | 1,506,108 |

| EMEA | 427,700 | 484,279 | 539,843 | 563,128 | 580,284 |

| Asia Pacific | 155,699 | 185,667 | 210,181 | 220,027 | 235,356 |

| Consolidated | 1,591,445 | 1,843,892 | 2,085,508 | 2,203,056 | 2,321,748 |

Source: Note 15, Segment Information — reportable geographic segments (Americas, EMEA, Asia Pacific) [5] [6] [7] [8]. Click any linked figure to open the filing page with the row highlighted.

Operating Income by Geographic Segment

| Operating Income by Geographic Segment | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Americas | 218,180 | 159,140 | 239,438 | 261,790 | 305,963 |

| EMEA | 159,704 | 196,231 | 243,028 | 282,963 | 274,002 |

| Asia Pacific | 96,157 | 120,111 | 146,741 | 156,546 | 168,338 |

| Consolidated | 474,041 | 475,482 | 629,207 | 701,299 | 748,303 |

Source: Note 15, Segment Information — results of operations of our segments [5] [6] [7] [8]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Income [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-17. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [9] [10] [11] [12]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows [13] [14] [15] [16]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income | Diluted earnings per common share | Net cash provided by operating activities |

|---|---|---|---|---|---|

| FY2016 | — | 349,676 | 338,815 | 8.19 | 331,140 |

| FY2017 | — | 352,135 | 258,259 | 6.51 | 320,527 |

| FY2018 | 1,350,145 | 366,204 | 267,085 | 6.78 | 385,668 |

| FY2019 | 1,435,351 | 438,035 | 352,790 | 9.08 | 427,136 |

| FY2020 | 1,494,111 | 439,660 | 372,938 | 9.65 | 505,840 |

| FY2021 | 1,591,445 | 474,041 | 399,590 | 10.36 | 555,226 |

| FY2022 | 1,843,892 | 475,482 | 396,917 | 10.25 | 538,277 |

| FY2023 | 2,085,508 | 629,207 | 468,173 | 12.04 | 645,573 |

| FY2024 | 2,203,056 | 701,299 | 537,126 | 13.91 | 700,338 |

| FY2025 | 2,321,748 | 748,303 | 597,040 | 15.55 | 726,260 |

Source: consolidated statements across filings; older years from the standardized feed [13] [1] [14] [2]. Click any linked figure to open the filing page with the row highlighted.

Operating KPIs

| KPI | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Annual Subscription Value (ASV), as reported | — | — | — | 2,255,400 | 2,405,600 |

| Organic ASV | — | — | — | — | 2,370,900 |

| ASV plus Professional Services, as reported | 1,688,300 | 2,027,400 | 2,174,600 | 2,276,000 | — |

| Total Clients with ASV over $10,000 | 6,453 | 7,538 | 7,921 | 8,217 | 8,996 |

| Total Users | — | — | — | 216,381 | 237,324 |

Source: company-reported operating metrics [17]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-17. Estimate figures link to the consensus source, not to filing pages.

Traceability

412 of 449 figures on this page (92%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

Display unit is thousands of US dollars (US$ thousands), exactly as FactSet's consolidated statements are printed ('in thousands, except per share data'). Per-share and KPI-count rows are exempt from that scale.

FactSet's fiscal year ends August 31. Each fiscal year is cited to its own Form 10-K (FY2021–FY2025); every value in the five annual statement columns is verified against the cited filing page.

Income statement presentation drift: the FY2022, FY2023 and FY2024 10-Ks break out an 'Asset impairments' line below SG A; the FY2021 and FY2025 10-Ks (and the standardized data feed) fold it into SG A. This tab shows each year's own-10-K presentation, so 'Asset impairments' is $0 in FY2021/FY2025 and SG A for FY2023/FY2024 differs from the data feed (see discrepancies).

In FY2021 and FY2022 the income statement reported interest on a net basis ('Interest expense, net'); FY2023 onward splits Interest income and Interest expense. The Interest income/Interest expense rows are therefore blank for FY2021–FY2022, while 'Total other income (expense), net' is populated for every year.

Revenue and operating income by geographic segment are taken from the Segment Information note (Note 15) of each year's 10-K, which reports Americas, EMEA and Asia Pacific as the reportable segments; the FY2021–FY2022 10-Ks label the row 'Revenue' (singular) and FY2023 onward 'Revenues'.

FY2016–FY2020 figures in the Long-Term Record are from the standardized data feed (SEC XBRL) and are shown without page links (those filings are not in the corpus); FY2016–FY2017 total revenue is not carried by the feed. FY2021–FY2025 long-term figures are verified to the filings.

Quarterly cash-flow single quarters are derived from the printed year-to-date statements in each Form 10-Q (Q1 as printed; Q2 = 6-month YTD minus Q1 3-month YTD; Q3 = 9-month YTD minus 6-month YTD). Every derived value reconciles exactly to the two printed YTD figures and was cross-checked against the quarterly data feed.

KPIs: FY2025 ASV and Organic ASV are cited to the FY2025 10-K (MD A, in $ millions; shown here rescaled to thousands). Other ASV, client-count (clients with ASV $10,000) and user-count figures are from the fiscal.ai data feed and are shown without page links — the 10-Ks disclose these only in rounded prose (e.g. '~9,000 clients', 'over 237,000 investment professionals'). The subscription metric's definition changed across years (ASV plus Professional Services through FY2024; ASV headline from FY2025).

2 figure(s) differed between the data feed and the filing; the filing value is shown (see the run's metrics/metrics_tab.json for the audit trail).

FactSet Research Systems Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Q3 FY2026 Earnings Presentation — Q3 FY2026

FactSet's fullest current self-portrait: what the platform is, how it grows, its scale and segment mix, and the FY26 margin picture. · Open the full document →

Q2 FY2026 Earnings Presentation — Q2 FY2026

Explains the moat and the FY26 investment cycle: why the data is hard to leave, how the analytics work, and where money is going. · Open the full document →

More from management

Q1 FY2026 Earnings Presentation — Q1 FY2026 · 25 pages · The first deck of the FY26 strategy reset; introduces the same foundational-strengths and investment framework at the year's start. · Open →

Q4 & Full-Year FY2025 Earnings Presentation — Q4 / FY2025 · 23 pages · Full-year FY2025 results, the multi-decade track record, and the FY2026 outlook that later quarters are measured against. · Open →

FactSet Research Systems Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

FactSet Research Systems — FY2025 Annual Report (Form 10-K) — FY2025 (year ended Aug 31, 2025)

The latest 10-K: subscription model, the Sep-2025 CEO handoff, and a still-open IT material weakness. · Open the full document →

Item 1. Business — p. 7 · Read the full section →

Management's own framing of the platform, its client base, and the three-segment / firm-type structure.

Self-description: a subscription platform serving ~9,000 clients and over 237,000 professionals.

FactSet is a global financial digital platform and enterprise solutions provider with open and flexible technologies that deliver financial intelligence to investment professionals worldwide. […] As of August 31, 2025, we had approximately 9,000 clients comprised of over 237,000 investment professionals, including institutional asset managers, bankers, wealth managers, asset owners, partners, hedge funds, corporate users, and private equity and venture capital professionals. Our revenues are primarily derived from subscriptions to our multi-asset class data and solutions powered by our connected data and technology platform. Our products and services include workstations, portfolio analytics and enterprise data solutions.

p. 7 · Read in context →

Executive Leadership Transition — p. 11 · Read the full section →

A leadership change dated after fiscal year-end — the reader's first flag of a new strategic hand on the tiller.

Sanoke Viswanathan became CEO on Sep 8, 2025, succeeding retiring Philip Snow.

On September 8, 2025, Sanoke Viswanathan assumed the role of Chief Executive Officer and joined FactSet’s Board of Directors. Mr. Viswanathan succeeds F. Philip Snow, who retired from these roles effective on Mr. Viswanathan's start date. To support a smooth leadership transition, Mr. Snow is continuing employment with FactSet in an advisory capacity until December 31, 2025.

p. 11 · Read in context →

Revenues and Annual Subscription Value ("ASV") — p. 11 · Read the full section →

How FactSet actually makes money — recurring subscriptions measured by ASV, with the retention rate that underpins it.

The Competitive Landscape — p. 12 · Read the full section →

Management names its rivals — useful for sizing the moat against far larger data vendors.

Largest competitors: Bloomberg, S&P Market Intelligence, LSEG (Refinitiv); also Aladdin, MSCI, Morningstar.

Our largest competitors are Bloomberg L.P., S&P's Market Intelligence division, and London Stock Exchange Group's ("LSEG's") Data & Analytics division (formerly known as Refinitiv). Other competitors and competitive products include online database suppliers and integrators and their applications, such as BlackRock Aladdin, MSCI Inc. and Morningstar Inc. Many of these firms provide products or services similar to our offerings.

p. 12 · Read in context →

Item 1A. Risk Factors — p. 21 · Read the full section →

Two structural, company-specific risks that could genuinely bite: AI disruption and the active-to-passive shift.

AI risk: may not generate revenue from AI investment, and rivals may adopt it faster.

We use, and are expanding our use of, machine learning and AI technologies in our products and processes. If we fail to keep pace with rapidly evolving AI technological developments, or fail to launch products that are competitive, our competitive position and business results may be negatively impacted. If our competitors or other third parties incorporate AI technologies, such as emerging generative and agentic AI, into their products and processes more quickly or more successfully than us, this could impair our ability to compete effectively. Our use of AI technologies, including generative and agentic AI, requires resources to develop, test and maintain such products, which is costly. Despite our investments in, and commitment of resources to, the development of AI products and technologies, we may not be successful in generating revenues from these efforts.

p. 25 · Read in context →

A continued shift to passive investing could reduce demand for FactSet's active-manager clients.

A continued shift to passive investing, resulting in an increased outflow to passively managed index funds, could reduce demand for the services of active investment managers[…]

p. 27 · Read in context →

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations — p. 45 · Read the full section →

Where management explains what drove fiscal 2025 — revenue, margin and EPS — plus the Organic ASV bridge.

Fiscal 2025: revenue +5.4% to $2,321.7M; net income +11.2%; Diluted EPS $15.55, +11.8%.

Revenues for fiscal 2025 were $2,321.7 million, an increase of 5.4% from the comparable prior year. The growth in revenues was driven by a 4.4% increase in organic revenues, a 0.9% increase from acquisition-related revenues and a net increase of 0.1% from foreign currency exchange rate fluctuations. Revenues increased in all our segments, primarily in the Americas. […] Net income for fiscal 2025 was $597.0 million, an increase of 11.2% from the prior year. Diluted earnings per common share ("Diluted EPS") for fiscal 2025 was $15.55, an increase of 11.8% compared with the prior year.

p. 47 · Read in context →

Item 9A. Controls and Procedures — p. 141 · Read the full section →

The standout governance flag — disclosure controls were not effective; a prior IT material weakness remains open.

Controls deemed not effective; the FY2024 IT general-controls material weakness continues, not fully remediated.

Our Principal Executive Officer and Principal Financial Officer have concluded that our disclosure controls and procedures were not effective as of the end of the annual period covered by this report due to a material weakness in internal control over financial reporting. This conclusion is due to a material weakness identified in the operation of certain key IT general controls. […] As reported in Part II, Item 9A. “Controls and Procedures” of our Annual Report on Form 10-K for the fiscal year ended August 31, 2024, we had identified a material weakness in the design and operation of IT general controls that support our revenues, accounts receivable, and deferred revenues processes which, in the aggregate, gave rise to a material weakness in internal control over financial reporting. While we have made significant progress remediating those control deficiencies, there remains certain deficiencies related to program change management and monitoring and user access in connection with segregation of duties and restrictions to appropriate users.

p. 141 · Read in context →

FactSet Research Systems — FY2024 Annual Report (Form 10-K) — FY2024 (year ended Aug 31, 2024)

Included to show where the material weakness originated — first disclosed here, with remediation promised for fiscal 2025. · Open the full document →

Item 9A. Controls and Procedures — p. 153 · Read the full section →

The first identification of the IT general-controls material weakness — read against FY2025 to see it left unresolved.

More annual reports

FactSet Research Systems — FY2023 Annual Report (Form 10-K) — FY2023 (year ended Aug 31, 2023) · 153 pages · Pre-material-weakness baseline under the Snow-era strategy and firm-type structure. · Open →

FactSet Research Systems — FY2022 Annual Report (Form 10-K) — FY2022 (year ended Aug 31, 2022) · 162 pages · First full year integrating the CGS (CUSIP Global Services) acquisition. · Open →

FactSet Research Systems — FY2021 Annual Report (Form 10-K) — FY2021 (year ended Aug 31, 2021) · 154 pages · Earliest edition on file — useful anchor for five-year ASV and margin trend. · Open →

Competitors describe FactSet Research Systems Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

S&P Global (SPGI)

The most direct desktop-and-data rival: S&P Capital IQ Pro competes seat-for-seat with the FactSet Workstation, and the two firms are named peers — S&P even sold its CUSIP business to FactSet.

S&P Global's stated view that its Capital IQ Pro desktop is growing faster than the underlying end market — the segment where it contests FactSet Workstation seats.

Martina Cheung, President & CEO: The Capital IQ Pro desktop continues to perform strongly and actually it's growing faster than the end market. And so we're very focused on our execution.

p. 13 · Read in context →

A direct link between the two rivals: S&P Global divested CUSIP Global Services out of its Market Intelligence segment to FactSet for $1.925bn (completed March 2022).

In March of 2022, we completed the previously announced sale of CUSIP Global Services (“CGS”), a business within our Market Intelligence segment, to FactSet Research Systems Inc. for a purchase price of $1.925 billion in cash, subject to customary adjustments.

p. 78 · Read in context →

London Stock Exchange Group (LSEG)

Owner of Refinitiv, whose Workspace desktop and data feeds are the other head-on rival to FactSet's Workstation and content business; LSEG frames itself as a share-taking data challenger.

An analyst's characterisation — undisputed by management — that LSEG has climbed from #6 to #3 in pricing & reference data (55% of Data & Feeds revenue), an adjacent feeds market FactSet also serves.

Russell Quelch, Rothschild & Co (analyst): You disclosed that 55% of the Data & Feeds revenues come from pricing and reference services. I believe you've gone from number 6 player there to number 3 player in the last couple of years, just behind ICE and Bloomberg.

p. 30 · Read in context →

LSEG's CEO concedes its Workspace desktop is priced at roughly a 30% discount to the 'big competitor' terminal — a pricing backdrop for the crowded desktop market FactSet also competes in.

David Schwimmer, CEO: The way I've answered an aspect of this question over the years, people ask us about the discount of, for example, our desktop product or Workspace relative to one of the big competitors and that being at a 30% or so discount, and we've always been clear we're never going to take the price up 29% in the new year.

p. 46 · Read in context →

LSEG's stated Microsoft-partnership roadmap: embedding Workspace data into Teams and Office 365 workflows via natural-language prompts — the same AI-plus-workflow terrain FactSet is targeting.

The first iteration of our Workspace for Teams application is now live with target customers, and we will be adding new functionalities and expanding the customer rollout over time. Integrating Workspace data into Teams enhances the discoverability of our data and insights by making them accessible in customers’ existing Office 365 workflow. Using simple prompts in Teams Chat, users can call up 20 different data sets with insights on bonds, equities, news, M&A league tables and so on, and share this information with ease.

p. 27 · Read in context →

MSCI (MSCI)

Names FactSet directly as an Analytics competitor; its Barra risk models and multi-asset portfolio analytics collide with FactSet's analytics and risk franchise.

MSCI's 10-K names FactSet Research Systems among the rivals to its Analytics business — an explicit head-to-head acknowledgement in multi-asset risk and portfolio analytics.

Analytics. Our Analytics offerings compete with those from a range of competitors, including Axioma (part of SimCorp), BlackRock Solutions, Bloomberg, and FactSet Research Systems Inc. Additionally, some of the larger broker-dealers have developed proprietary analytics tools for their clients.

p. 19 · Read in context →

MSCI quantifies momentum in the FactSet-competing Analytics segment: high-single-digit run-rate growth and new recurring sales up 30% year-over-year, with enterprise risk and performance wins.

Andy Wiechmann, CFO: In Analytics, run rate growth was in the high single digits, driven by new recurring sales of $17 million, which grew 30% from a year ago. We saw continued strength in equity Analytics, and we had some large enterprise risk and performance wins.

p. 3 · Read in context →

MSCI's stated workflow-lock-in narrative — Barra equity-factor and enterprise risk tools 'deeply embedded' in hedge-fund workflows — the retention story that most directly rivals FactSet's analytics value proposition.

Baer Pettit, President & COO: we see ongoing strong demand from hedge funds for MSCI's equity factor and enterprise risk and performance solutions, which have become deeply embedded in many clients' investment workflows. For example, MSCI closed a 7-figure renewal deal with one of the world's largest hedge funds in which our contribution to their alpha generation and risk management is central.

p. 2 · Read in context →

Morningstar (MORN)

Names FactSet as a competitor across three fronts — the Morningstar Direct workstation, PitchBook private-market data, and Advisor Workstation — the closest multi-product mirror of FactSet's desktop-and-data model.

Morningstar lists FactSet (Cognity and SPAR) among the primary global competitors to Morningstar Direct, its multi-asset analysis and reporting workstation — the direct analogue to the FactSet Workstation.

Its key global competitors are Bloomberg, eVestment Alliance, FactSet Research System’s Cognity and SPAR, and LSEG's (Refinitiv) Eikon.

p. 7 · Read in context →

In private-market data and workflow tools (PitchBook), Morningstar again names FactSet among key competitors; the same page discloses ~10,200 client accounts and 113,451 licensed users at year-end 2025.

We compete with providers of private market data, research, and workflow tools. Key competitors include Beauhurst, FactSet, MSCI, Preqin (a division of BlackRock), Refinitiv, S&P Global Market Intelligence, and smaller or specialized data providers.

p. 11 · Read in context →

For its advisor-facing workstation (reaching 170,000+ advisors across 225+ firms in the US and Canada), Morningstar again lists FactSet among competitors.

Morningstar Advisor Workstation is offered in the US and Canada, reaching more than 225 firms and 170,000 advisors. […] Competitors for Morningstar Advisor Workstation include CapIntel, FactSet, Kwanti, Nitrogen (formerly known as Riskalyze), and YCharts.

p. 9 · Read in context →

Moody's (MCO)

Through the Moody's Analytics segment — research, data and cloud workflow tools sold on a subscription/ARR model — Moody's competes for the same research-feed and analytics budgets as FactSet.

Moody's Analytics sizes its recurring book at $3.6bn ARR (+8% YoY) with mid-to-high-single-digit growth across research and data lines — the subscription model that overlaps FactSet's ASV base.

Noemie Heuland, CFO: ARR ended Q1 at $3.6 billion, up 8% year-over-year. Decision Solutions continues to be a key growth engine for MA, representing approximately 44% of total MA ARR and delivering 10% ARR growth.

p. 3 · Read in context →

Moody's reports a 97% trailing-12-month retention rate framed as workflow embeddedness — the same high-renewal moat FactSet claims for its own subscription base.

Robert Fauber, CEO: That growth was also supported by our trailing 12-month retention rate of 97%, which reflects how embedded we are in customers' workflows as what they call their primary view of risk.

p. 2 · Read in context →

BlackRock (BLK)

Competes with FactSet solely through its Aladdin technology platform — end-to-end portfolio and risk analytics sold to institutions — a far larger tech-ARR franchise overlapping FactSet's analytics and workflow offering.

BlackRock's stated Aladdin roadmap — GenAI 'AI copilots,' open ecosystem connectivity and whole-portfolio public/private analytics — maps onto the vectors where Aladdin encroaches on FactSet's analytics and workflow domain.

Investments in Aladdin AI copilots, enhancements in openness supporting ecosystem partnerships, and advancing whole portfolio solutions including private markets and digital assets are expected to further augment the value of using Aladdin.

p. 54 · Read in context →

More peer documents

S&P Global FY2025 10-K — Market Intelligence segment & M&A — 220 pages · Market Intelligence described as 'multi-asset-class data and analytics integrated with purpose-built workflow solutions'; lists the Capital IQ Pro build-out (Visible Alpha, ChartIQ, ProntoNLP) and names FactSet in the stock-performance peer group (p.58). · Open →

S&P Global Q2 FY2025 call — competitive displacements & retention — 16 pages · Cheung reports net renewal rate up >1pt YoY, a Barclays enterprise deal 'powered by Capital IQ Pro,' and Q&A on competitive displacements and Visible Alpha integration. · Open →

Morningstar FY2024 10-K — prior-year FactSet naming — 204 pages · Names FactSet as a rival in market/equity data (p.9) and Morningstar Direct (p.11) with prior-year renewal-rate comparatives, showing the framing is persistent — but note methodology was restated in FY2025. · Open →

Moody's Analytics Q3 FY2025 call — GenAI product build-out — 13 pages · Fauber details 20+ standalone/AI-enabled applications and 50+ domain-specific agents on proprietary data — the GenAI-research push that collides with FactSet's AI roadmap. · Open →

Moody's FY2025 10-K — Analytics segment financials — 197 pages · Moody's Analytics external revenue $3,599m (+9%), split Decision Solutions $1,692m / Research & Insights $995m / Data & Information $912m (p.74) for sizing the FactSet-competing segment. · Open →

BlackRock Q1 FY2026 call — Aladdin + Preqin private-markets push — 12 pages · Fink pitches Aladdin+eFront+Preqin as 'the language of private credit portfolios,' and CFO Small anchors long-term low-to-mid-teens ACV growth — the private-markets-data land grab overlapping FactSet. · Open →

Source: S&P Capital IQ consensus via Xpressfeed · Generated 2026-07-17.

Street snapshot

Sixteen price targets span $210 to $340 (mean $254, median $246.5), a wide band around a stock the Street rates cautiously.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst counts shown explicitly; recommendation respondents: 18.

| Street view | Reading | Analysts |

|---|---|---|

| Recommendation mix | Buy 2, Outperform 0, Hold 10, Underperform 2, Sell 4 | 18 |

| Consensus score | 3.33 | 18 |

| Target price | mean 254.0; high 340.0; low 210.0 | 16 |

Forward table

Consensus carries revenue from FY2025's $2,321.7M actual to roughly $2,769M by FY2028 and normalized EPS from $16.98 to about $21.87, i.e. steady mid-single-digit revenue growth with a faster EPS climb. Gross margin is modeled to ease toward 51% in FY2026 from 53.4% in FY2025.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst count is the estimate count for each period and metric.

| Period | Metric | Mean | YoY | Analysts | Low / high |

|---|---|---|---|---|---|

| FY0E | Revenue | 2,470 | 6.4% | 16 | 2,453 / 2,475 |

| FY0E | EBITDA | 923.4 | -1.2% | 10 | 872.0 / 943.0 |

| FY0E | EBIT | 850.9 | 0.3% | — | — / — |

| FY0E | Net income (GAAP) | 554.0 | -7.2% | 10 | 541.7 / 567.5 |

| FY0E | Net income (normalized) | 654.1 | -0.2% | — | — / — |

| FY0E | EPS (GAAP) | 15.06 | -3.1% | 11 | 14.78 / 15.44 |

| FY0E | EPS (normalized) | 17.81 | 4.9% | 18 | 17.49 / 18.01 |

| FY0E | Free cash flow | 691.3 | 6.1% | — | — / — |

| FY0E | Dividend per share | 4.49 | 5.4% | — | — / — |

| FY0E | Gross margin | 51.3% | -3.9% | — | — / — |

| FY0E | Capital expenditure | -116.2 | 16.7% | — | — / — |

| FY0E | Net debt | 1,057 | -0.5% | — | — / — |

| FY0E | Cash from operations | 809.4 | 5.2% | — | — / — |

| FY0E | ROE | 26.5% | -7.4% | — | — / — |

| FY+1E | Revenue | 2,613 | 5.8% | 16 | 2,575 / 2,634 |

| FY+1E | EBITDA | 998.3 | 8.1% | 10 | 936.4 / 1,046 |

| FY+1E | EBIT | 900.7 | 5.8% | — | — / — |

| FY+1E | Net income (GAAP) | 627.5 | 13.3% | 10 | 604.3 / 649.0 |

| FY+1E | Net income (normalized) | 691.1 | 5.7% | — | — / — |

| FY+1E | EPS (GAAP) | 17.81 | 18.3% | 11 | 16.63 / 18.67 |

| FY+1E | EPS (normalized) | 19.67 | 10.5% | 18 | 18.62 / 20.30 |

| FY+1E | Free cash flow | 711.4 | 2.9% | — | — / — |

| FY+1E | Dividend per share | 4.72 | 5.1% | — | — / — |

| FY+1E | Gross margin | 51.8% | 1.0% | — | — / — |

| FY+1E | Capital expenditure | -127.7 | 9.8% | — | — / — |

| FY+1E | Net debt | 851.2 | -19.4% | — | — / — |

| FY+1E | Cash from operations | 865.8 | 7.0% | — | — / — |

| FY+1E | ROE | 29.9% | 12.9% | — | — / — |

| FY+2E | Revenue | 2,769 | 6.0% | 13 | 2,693 / 2,818 |

| FY+2E | EBITDA | 1,050 | 5.2% | 8 | 947.7 / 1,126 |

| FY+2E | EBIT | 953.8 | 5.9% | — | — / — |

| FY+2E | Net income (GAAP) | 685.4 | 9.2% | 7 | 645.4 / 712.0 |

| FY+2E | Net income (normalized) | 736.9 | 6.6% | — | — / — |

| FY+2E | EPS (GAAP) | 19.96 | 12.1% | 8 | 17.77 / 20.82 |

| FY+2E | EPS (normalized) | 21.87 | 11.2% | 14 | 19.88 / 23.17 |

| FY+2E | Free cash flow | 748.3 | 5.2% | — | — / — |

| FY+2E | Dividend per share | 4.94 | 4.8% | — | — / — |

| FY+2E | Gross margin | 51.7% | -0.2% | — | — / — |

| FY+2E | Capital expenditure | -136.1 | 6.6% | — | — / — |

| FY+2E | Net debt | 818.4 | -3.9% | — | — / — |

| FY+2E | Cash from operations | 929.6 | 7.4% | — | — / — |

| FY+2E | ROE | 32.1% | 7.2% | — | — / — |

| Q4 FY2026 | Revenue | 629.2 | 5.4% | 14 | 625.8 / 633.6 |

| Q4 FY2026 | EBITDA | 231.3 | -5.4% | 7 | 219.6 / 241.0 |

| Q4 FY2026 | EBIT | 206.9 | -0.3% | — | — / — |

| Q4 FY2026 | Net income (GAAP) | 139.0 | -9.5% | 8 | 129.3 / 153.8 |

| Q4 FY2026 | Net income (normalized) | 155.0 | -1.3% | — | — / — |

| Q4 FY2026 | EPS (GAAP) | 3.91 | -3.0% | 9 | 3.62 / 4.29 |

| Q4 FY2026 | EPS (normalized) | 4.34 | 7.1% | 16 | 4.14 / 4.52 |

| Q4 FY2026 | Free cash flow | 166.4 | -6.8% | — | — / — |

| Q4 FY2026 | Dividend per share | 1.14 | 3.6% | — | — / — |

| Q4 FY2026 | Gross margin | 51.1% | -3.7% | — | — / — |

| Q4 FY2026 | Capital expenditure | -28.83 | 12.3% | — | — / — |

| Q4 FY2026 | Net debt | 1,008 | — | — | — / — |

| Q4 FY2026 | ROE | 27.7% | 6.1% | — | — / — |

| Q4 FY2026 | Cash from operations | 207.5 | -8.5% | — | — / — |

| Q1 FY2027 | Revenue | 643.2 | 5.9% | 12 | 637.8 / 649.4 |

| Q1 FY2027 | EBITDA | 252.6 | 2.0% | 6 | 243.4 / 259.0 |

| Q1 FY2027 | EBIT | 228.2 | 6.7% | — | — / — |

| Q1 FY2027 | Net income (GAAP) | 156.8 | 2.8% | 6 | 150.5 / 162.2 |

| Q1 FY2027 | Net income (normalized) | 173.5 | 5.2% | — | — / — |

| Q1 FY2027 | EPS (GAAP) | 4.46 | 9.8% | 7 | 4.28 / 4.64 |

| Q1 FY2027 | EPS (normalized) | 4.94 | 9.5% | 15 | 4.75 / 5.14 |

| Q1 FY2027 | Free cash flow | 124.6 | 2.4% | — | — / — |

| Q1 FY2027 | Dividend per share | 1.15 | 2.5% | — | — / — |

| Q1 FY2027 | Gross margin | 52.5% | -1.5% | — | — / — |

| Q1 FY2027 | Capital expenditure | -29.44 | 8.1% | — | — / — |

| Q1 FY2027 | Net debt | 893.5 | — | — | — / — |

| Q1 FY2027 | ROE | 30.8% | 13.5% | — | — / — |

| Q1 FY2027 | Cash from operations | 137.5 | -5.6% | — | — / — |

| Q2 FY2027 | Revenue | 647.0 | 5.9% | 12 | 641.2 / 650.7 |

| Q2 FY2027 | EBITDA | 248.9 | 14.3% | 6 | 236.5 / 258.0 |

| Q2 FY2027 | EBIT | 223.5 | 4.3% | — | — / — |

| Q2 FY2027 | Net income (GAAP) | 154.6 | 16.2% | 6 | 148.5 / 160.8 |

| Q2 FY2027 | Net income (normalized) | 169.9 | 4.6% | — | — / — |

| Q2 FY2027 | EPS (GAAP) | 4.43 | 23.3% | 7 | 4.25 / 4.67 |

| Q2 FY2027 | EPS (normalized) | 4.90 | 9.8% | 15 | 4.68 / 5.07 |

| Q2 FY2027 | Free cash flow | 179.4 | 8.4% | — | — / — |

| Q2 FY2027 | Dividend per share | 1.15 | 4.4% | — | — / — |

| Q2 FY2027 | Gross margin | 51.5% | -1.1% | — | — / — |

| Q2 FY2027 | Capital expenditure | -27.76 | -3.2% | — | — / — |

| Q2 FY2027 | Net debt | 712.9 | -30.4% | — | — / — |

| Q2 FY2027 | ROE | 29.2% | 7.5% | — | — / — |

| Q2 FY2027 | Cash from operations | 218.9 | 8.3% | — | — / — |

| Q3 FY2027 | Revenue | 659.3 | 5.8% | 12 | 653.8 / 664.5 |

| Q3 FY2027 | EBITDA | 250.3 | 17.1% | 6 | 233.5 / 270.3 |

| Q3 FY2027 | EBIT | 226.2 | 5.6% | — | — / — |

| Q3 FY2027 | Net income (GAAP) | 155.1 | 22.4% | 6 | 145.9 / 160.0 |

| Q3 FY2027 | Net income (normalized) | 171.9 | 5.4% | — | — / — |

| Q3 FY2027 | EPS (GAAP) | 4.48 | 27.9% | 7 | 4.23 / 4.75 |

| Q3 FY2027 | EPS (normalized) | 4.93 | 8.9% | 15 | 4.70 / 5.15 |

| Q3 FY2027 | Free cash flow | 207.2 | -0.2% | — | — / — |

| Q3 FY2027 | Dividend per share | 1.17 | 2.8% | — | — / — |

| Q3 FY2027 | Gross margin | 50.6% | -1.3% | — | — / — |

| Q3 FY2027 | Capital expenditure | -29.56 | 11.7% | — | — / — |

| Q3 FY2027 | Net debt | 570.0 | -44.9% | — | — / — |

| Q3 FY2027 | Cash from operations | 265.1 | 13.6% | — | — / — |

| Q3 FY2027 | ROE | 28.0% | 1.1% | — | — / — |

Estimate momentum

Out-year consensus has firmed over the past 180 days: FY2027 revenue moved from $2,578.8M to $2,613.0M and normalized EPS from $19.01 to $19.67, with FY2028 estimates similarly higher. The revisions are broad across both years and metrics but modest in size.

Currency: USD · Scale: money in millions, absolute (per share) · Point-in-time consensus; analyst count is shown where supplied.

| Period | Metric | Lookback | Then | Now | Direction / magnitude | Analysts |

|---|---|---|---|---|---|---|

| 2027 | Revenue | 30d | 2,604 | 2,613 | up 0.4% | — |

| 2027 | Revenue | 90d | 2,603 | 2,613 | up 0.4% | — |

| 2027 | Revenue | 180d | 2,579 | 2,613 | up 1.3% | — |

| 2028 | EPS (normalized) | 30d | 21.44 | 21.87 | up 2.0% | — |

| 2028 | EPS (normalized) | 90d | 21.48 | 21.87 | up 1.8% | — |

| 2028 | EPS (normalized) | 180d | 20.95 | 21.87 | up 4.4% | — |

| 2028 | Revenue | 30d | 2,755 | 2,769 | up 0.5% | — |

| 2028 | Revenue | 90d | 2,754 | 2,769 | up 0.5% | — |

| 2028 | Revenue | 180d | 2,725 | 2,769 | up 1.6% | — |

| 2027 | EPS (normalized) | 30d | 19.39 | 19.67 | up 1.5% | — |

| 2027 | EPS (normalized) | 90d | 19.42 | 19.67 | up 1.3% | — |

| 2027 | EPS (normalized) | 180d | 19.01 | 19.67 | up 3.5% | — |

Beat / miss record

Revenue has topped consensus in seven of the last eight quarters, the exception a fractional FY2025 Q2 miss.

Current sequences by metric: Revenue: 5 consecutive beats; EPS (normalized): 3 consecutive beats.

Currency: USD · Scale: money in millions, absolute (per share) · Consensus is captured before each actual first became effective; analyst count shown per observation.

| Quarter | Metric | Consensus as of | Actual | Surprise | Outcome | Analysts |

|---|---|---|---|---|---|---|

| Q3 FY2026 | Revenue | 618.1 | 622.9 | 0.8% | Beat | — |

| Q3 FY2026 | EPS (normalized) | 4.45 | 4.53 | 1.8% | Beat | — |

| Q2 FY2026 | Revenue | 604.9 | 611.0 | 1.0% | Beat | — |

| Q2 FY2026 | EPS (normalized) | 4.38 | 4.46 | 1.9% | Beat | — |

| Q1 FY2026 | Revenue | 600.6 | 607.6 | 1.2% | Beat | — |

| Q1 FY2026 | EPS (normalized) | 4.36 | 4.51 | 3.5% | Beat | — |

| Q4 FY2025 | Revenue | 593.4 | 596.9 | 0.6% | Beat | — |

| Q4 FY2025 | EPS (normalized) | 4.13 | 4.05 | -1.9% | Miss | — |

| Q3 FY2025 | Revenue | 580.9 | 585.5 | 0.8% | Beat | — |

| Q3 FY2025 | EPS (normalized) | 4.30 | 4.27 | -0.6% | Miss | — |

| Q2 FY2025 | Revenue | 570.7 | 570.7 | -0.0% | Miss | — |

| Q2 FY2025 | EPS (normalized) | 4.18 | 4.28 | 2.4% | Beat | — |

| Q1 FY2025 | Revenue | 565.0 | 568.7 | 0.6% | Beat | — |

| Q1 FY2025 | EPS (normalized) | 4.28 | 4.37 | 2.2% | Beat | — |

| Q4 FY2024 | Revenue | 546.8 | 562.2 | 2.8% | Beat | — |

| Q4 FY2024 | EPS (normalized) | 3.62 | 3.74 | 3.3% | Beat | — |

Where the street disagrees

Disagreement concentrates in the thinly-covered out-years: FY2029 rests on just five revenue estimates, five normalized-EPS estimates (stddev $1.58) and a single EBITDA mark, so those spreads carry a weak signal.

Currency: USD · Scale: money in millions, absolute (per share) · Dispersion is high-low divided by absolute mean; analyst count shown per item.

| Period | Metric | Mean | Low | High | Spread / mean | Analysts |

|---|---|---|---|---|---|---|

| 2029 | EPS (GAAP) | 21.99 | 18.83 | 23.80 | 22.6% | 4 |

| 2029 | EPS (normalized) | 23.96 | 21.04 | 25.55 | 18.8% | 5 |

| Q4 FY2026 | Net income (GAAP) | 139.0 | 129.3 | 153.8 | 17.6% | 8 |

| Q4 FY2026 | EPS (GAAP) | 3.91 | 3.62 | 4.29 | 17.2% | 9 |

| 2028 | EBITDA | 1,050 | 947.7 | 1,126 | 17.0% | 8 |

Source: Visible Alpha consensus via S&P Xpressfeed · Consensus as of 2026-07-15 · generated 2026-07-17.

Model trust

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Coverage depth and vintage; broker count is the maximum represented.

| Brokers | Line items | Last revision |

|---|---|---|

| 16 | 361 | 2026-07-15 |

Operating KPIs

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · FY-1A / FY0E / FY+1E; broker count shown per KPI.

| Operating KPI | Source | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|---|

| Depreciation and amortization | CD | 153,841.11bn Amount | 177,402.88bn Amount | 177,704.91bn Amount | 16 |

| Depreciation and amortization exp | CD | 154,141.50bn Amount | 177,402.69bn Amount | 177,704.91bn Amount | 16 |

| Dividend payments | CD | 163,290.08bn Amount | 164,682.67bn Amount | 168,114.01bn Amount | 16 |

| Long-term debt | CD | 1,362,454.00bn Amount | 1,084,222.25bn Amount | 1,046,872.25bn Amount | 16 |

| Net cash provided by/(used in) operating activities | CD | 779,452.70bn Amount | 810,713.12bn Amount | 865,740.18bn Amount | 16 |

| Purchases of property, equipment and leasehold improvements, net | CD | 99,403.55bn Amount | 118,981.64bn Amount | 121,040.77bn Amount | 16 |

| Repurchase of common stock | CD | 280,503.40bn Amount | 620,891.64bn Amount | 451,423.22bn Amount | 16 |

| Revenues | CD | 2,318,235.05bn Amount | 2,470,577.65bn Amount | 2,615,364.10bn Amount | 16 |

| Stock-based compensation expense | CD | 62,321.34bn Amount | 79,216.43bn Amount | 82,358.84bn Amount | 16 |

| Cash and cash equivalents | CD | 511,030.29bn Amount | 301,692.75bn Amount | 470,740.56bn Amount | 15 |

| Cost of services | CD | 1,090,097.57bn Amount | 1,206,073.75bn Amount | 1,266,689.18bn Amount | 15 |

| Free cash flow (FCF) | CD | 673,991.84bn Amount | 695,263.99bn Amount | 746,677.31bn Amount | 15 |

P&L bridge

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Margins are derived against revenue; YoY compares adjacent fiscal columns; broker count shown per line.

| P&L line | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|

| Revenue | 2,318,235.05bn Amount | 2,470,577.65bn Amount (6.6% YoY) | 2,615,364.10bn Amount (5.9% YoY) | 16 |

| Gross Profit | 1,228,157.31bn Amount (53.0% margin) | 1,264,537.12bn Amount (51.2% margin; 3.0% YoY) | 1,347,656.89bn Amount (51.5% margin; 6.6% YoY) | 15 |

| Ebitda | 984,743.24bn Amount (42.5% margin) | 1,007,006.91bn Amount (40.8% margin; 2.3% YoY) | 1,062,597.21bn Amount (40.6% margin; 5.5% YoY) | 15 |

| Operating Income | 849,630.19bn Amount (36.6% margin) | 848,704.63bn Amount (34.4% margin; -0.1% YoY) | 896,138.16bn Amount (34.3% margin; 5.6% YoY) | 16 |

| Net Income | 655,351.83bn Amount (28.3% margin) | 654,334.08bn Amount (26.5% margin; -0.2% YoY) | 690,116.96bn Amount (26.4% margin; 5.5% YoY) | 16 |

| Eps | 17.08 Amount | 17.83 Amount (4.4% YoY) | 19.65 Amount (10.2% YoY) | 16 |

Consensus dispersion

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Top high-low spreads relative to absolute mean; requires at least 3 brokers.

| Line item | Period | Mean | Min | Q1 | Q3 | Max | Spread / mean | Brokers |

|---|---|---|---|---|---|---|---|---|

| Dividend payments | 1QFY-2026 | 55,002.57bn Amount | 41,202.70bn Amount | 41,584.20bn Amount | 42,255.64bn Amount | 198,109.34bn Amount | 285.3% | 12 |

| Stock-based compensation expense | 4QFY-2025 | 14,680.43bn Amount | -17,154.00bn Amount | 17,015.00bn Amount | 17,801.48bn Amount | 21,094.84bn Amount | 260.5% | 12 |

| Cash and cash equivalents | FY-2028 | 596,654.97bn Amount | 138,241.86bn Amount | 374,194.41bn Amount | 770,719.26bn Amount | 1,511,759.93bn Amount | 230.2% | 13 |

| Repurchase of common stock | 2QFY-2026 | 117,240.04bn Amount | 55,000.00bn Amount | 78,851.58bn Amount | 128,238.75bn Amount | 300,000.00bn Amount | 209.0% | 11 |

| Cash and cash equivalents | FY-2027 | 470,740.56bn Amount | 162,163.93bn Amount | 326,307.53bn Amount | 523,327.75bn Amount | 1,032,553.80bn Amount | 184.9% | 14 |

| Cash and cash equivalents | 2QFY-2027 | 355,384.70bn Amount | 214,731.33bn Amount | 262,802.00bn Amount | 399,180.14bn Amount | 740,723.10bn Amount | 148.0% | 10 |

Quarterly path

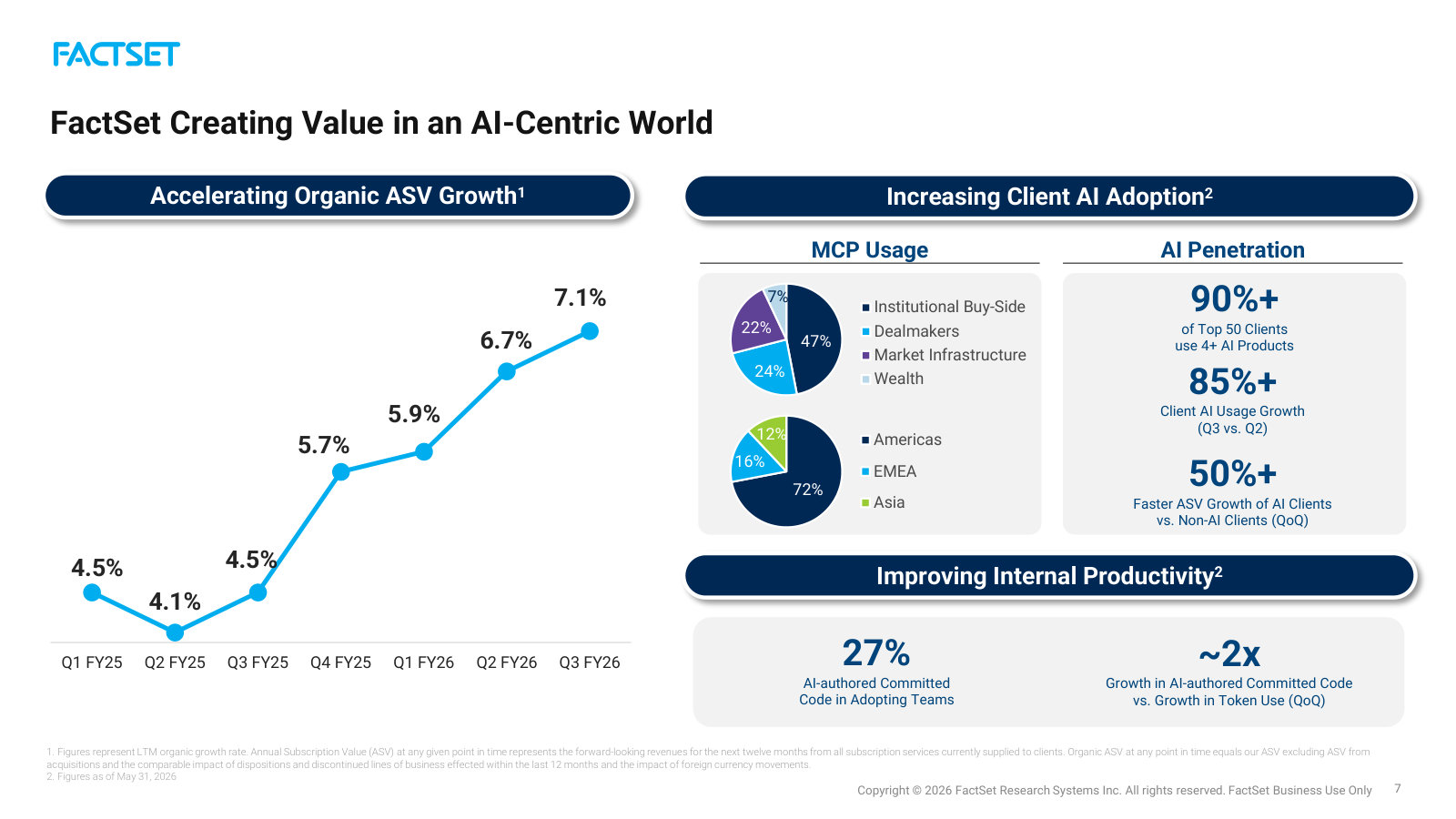

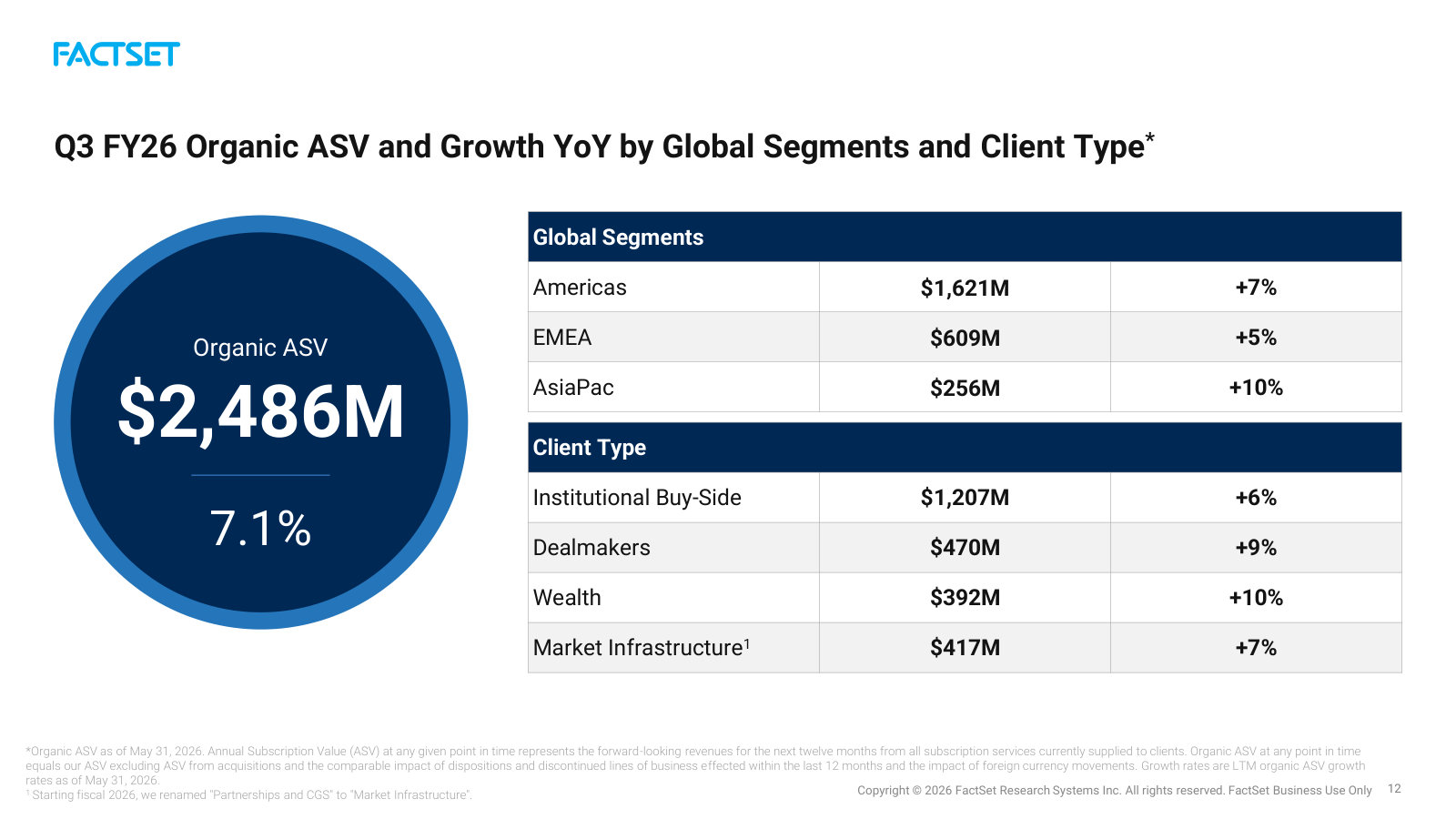

The ASV organic growth rate steps down modestly across the same quarters, from roughly 6.7% to 5.9%, a gentle deceleration rather than an inflection.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Next four supplied quarters; final column is maximum broker coverage in the row.

| Quarter | Depreciation and amortization | Depreciation and amortization exp | Dividend payments | Long-term debt | Net cash provided by/(used in) operating activities | Total revenue | EPS Diluted, Applicable to common stockholders($) | Broker coverage |

|---|---|---|---|---|---|---|---|---|

| 4QFY-2026 | 43,140.00bn Amount | 44,261.57bn Amount | 41,929.33bn Amount | 1,059,871.14bn Amount | 193,319.50bn Amount | 629,028.08bn Amount | 4.35 Amount | 16 |

| 1QFY-2027 | 43,402.99bn Amount | 43,655.67bn Amount | 42,168.64bn Amount | 1,022,906.15bn Amount | 163,715.16bn Amount | 641,428.35bn Amount | 4.91 Amount | 16 |

| 2QFY-2027 | 43,549.63bn Amount | 43,870.84bn Amount | 41,322.90bn Amount | 1,021,436.50bn Amount | 212,549.51bn Amount | 646,602.32bn Amount | 4.89 Amount | 15 |

| 3QFY-2027 | 44,243.70bn Amount | 44,537.19bn Amount | 42,341.09bn Amount | 1,008,936.50bn Amount | 272,162.40bn Amount | 659,379.73bn Amount | 4.94 Amount | 15 |

15 stale period values omitted; 1 line item fully removed.

Source: S&P Capital IQ transcripts via Xpressfeed · latest indexed call 2026-07-01 · generated 2026-07-17.

Latest call digest

FactSet Research Systems Inc., Q3 2026 Earnings Call, Jul 01, 2026 · 2026-07-01T13:00:00

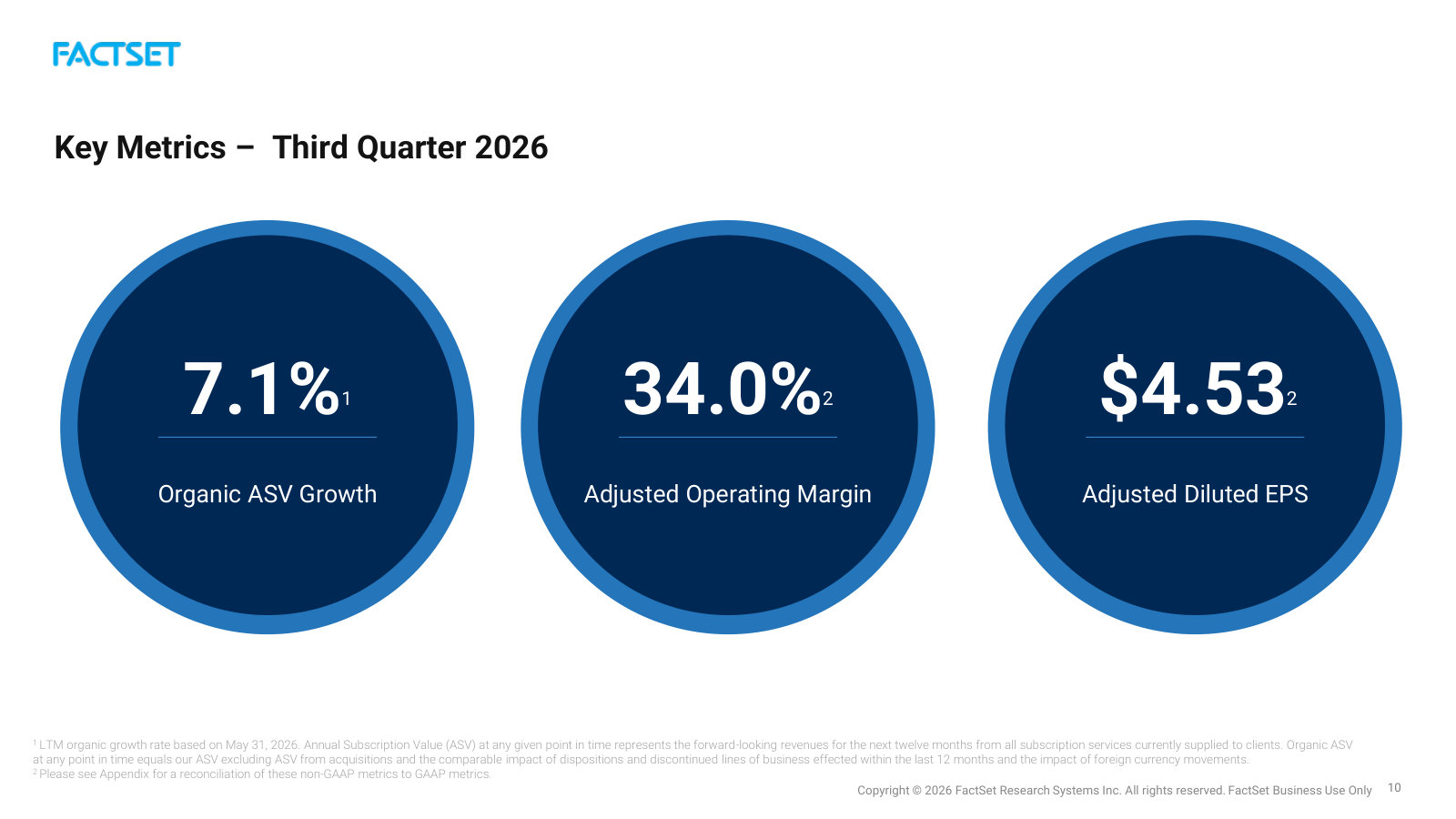

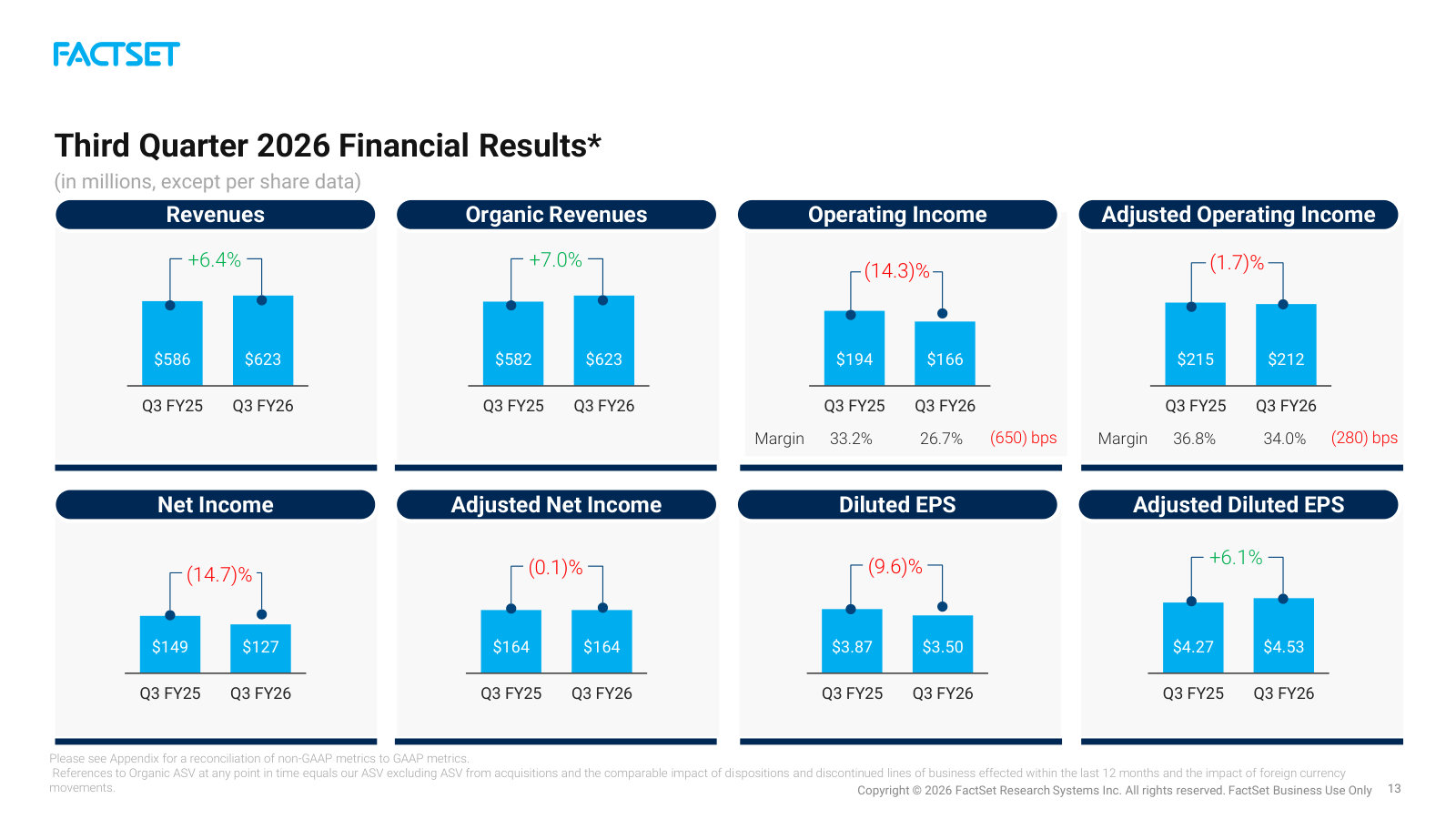

Q3 FY2026 call, July 1, 2026. FactSet reported its fifth straight quarter of accelerating organic ASV growth, up 7.1% to $2.48 billion across all regions and client types, with adjusted operating margin of 34% and adjusted diluted EPS of $4.53 (up 6.1%). This was Sanoke Viswanathan's fourth call as CEO and Joshua Warren's first as CFO, succeeding Helen Shan.

Prepared remarks leaned heavily on AI: over 90% of the top 50 clients now use four or more FactSet AI solutions, ASV growth among AI-adopting clients ran 50% higher than the rest of the book, MCP API call volume hit 13x the prior quarter, and management said more than 10% of ASV growth came directly from AI SKUs. Management also detailed productivity moves — coding agents now author 27% of committed code, and the company initiated a roughly 10% reduction in its technology workforce — alongside a new Google Cloud partnership and the FactSet Intelligence branding.

The Q&A reality was more skeptical. Analysts pressed on the guidance that implies Q4 moderation, on the 300 bp year-over-year margin decline and when leverage returns, on how AI actually monetizes beyond ASV optics, and on the +30% contract-term extension and whether price was traded for length. Management reaffirmed the previously raised FY2026 ranges and said revenue and EPS are tracking toward the high end, attributing the margin dip to performance-linked compensation and deliberate investment rather than headcount growth.

Participant coverage from the latest call.

| Group | Participants | Count |

|---|---|---|

| Management | Operator; Kevin Toomey — Head of Investor Relations, FactSet Research Systems Inc.; Sanoke Viswanathan — CEO & Director, FactSet Research Systems Inc.; Joshua Warren — Chief Financial Officer, FactSet Research Systems Inc. | 4 |

| Analysts | Ashish Sabadra — Analyst, RBC Capital Markets, Research Division; Faiza Alwy — Research Analyst, Deutsche Bank AG, Research Division; Alex Kramm — Executive Director and Equity Research Analyst of Exchanges, Ebrokers, UBS Investment Bank, Research Division; Kelsey Zhu — Financial Information Technology Analyst, Autonomous Research US LP; Manav Patnaik — MD, Business & Information Services Equity Research Analyst., Barclays Bank PLC, Research Division; Shlomo Rosenbaum — Managing Director, Stifel, Nicolaus & Company, Incorporated, Research Division; Surinder Thind — Equity Analyst, Jefferies LLC, Research Division; Yehuda Silverman — Research Associate, Morgan Stanley, Research Division; Andrew Nicholas — Analyst, William Blair & Company L.L.C., Research Division; Keen Fai Tong — Research Analyst, Goldman Sachs Group, Inc., Research Division; Jason Haas — Executive Director & Senior Equity Analyst, Wells Fargo Securities, LLC, Research Division; Curtis Nagle — Vice President, BofA Securities, Research Division | 12 |

Curated latest-call exchanges; one row per analyst topic.

| Analyst | Firm | Topic | What changed in Q&A |

|---|---|---|---|

| Ashish Sabadra | RBC Capital Markets | Guidance implying Q4 moderation | Asked whether the softer implied Q4 is conservatism or reflects specific puts and takes; management cited a tough compare against a record Q4 and reaffirmed guidance without raising it. |

| Faiza Alwy | Deutsche Bank | AI monetization mechanics | Pressed on how AI adoption actually converts to revenue; management pointed to ASV acceleration, MCP-driven upsell and >10% of ASV growth from AI SKUs rather than a discrete AI price. |

| Alex Kramm | UBS | Margin trajectory and one-time items | Questioned whether the midpoint margin target holds and which FY2026 one-off costs roll off into FY2027; management pointed to a clear line of sight on margin improvement but declined FY2027 specifics. |

| Shlomo Rosenbaum | Stifel | Contract-term extension and disclosure | Asked whether the ~30% longer contract terms traded away price and about lock-in risk, plus dropped client/user/employee metrics; management said no price compression and disclosed user count up 12%. |

| Jason Haas | Wells Fargo | Implied margin cadence | Noted the guided rest-of-year margin implies a sharp improvement versus the ~300 bp Q3 decline and asked about comp pull-forward; management framed it as retained flexibility to pay for ASV outperformance. |

| Curtis Nagle | BofA Securities | Token costs and returns | Asked to unpack the token-cost drag on margin and expected returns; CFO called token spend entirely net-new versus 2025 and described controls around routing and budgeting. |

Theme tracker

Themes are curator-classified across supplied calls.

| Theme | Status | Quarters mentioned | Read-through |

|---|---|---|---|

| Organic ASV re-acceleration | persisted | Q4 2025, Q1 2026, Q2 2026, Q3 2026 | Growth has accelerated for five consecutive quarters to 7.1%, reversing the FY2024 deceleration and becoming the central bull point management returns to each call. |

| AI monetization (gen AI to MCP to agentic FactSet Intelligence) | persisted | Q4 2025, Q1 2026, Q2 2026, Q3 2026 | AI moved from an early gen-AI narrative to concrete metrics — MCP launched in December, over 450 MCP clients, and management now credits AI for a rising share of ASV growth. The dominant and intensifying topic. |

| Investment-driven margin compression | persisted | Q4 2025, Q1 2026, Q2 2026, Q3 2026 | Second-half-weighted investment and performance-linked compensation have pressured adjusted operating margin (34% in Q3, down ~300 bp year-over-year); management repeatedly frames it as deliberate and reversible. |

| Shift to enterprise and consumption-based agreements | emerged | Q2 2026, Q3 2026 | Management describes a move away from seat-linked contracts toward multi-year enterprise agreements with minimum commitments and consumption upside; contract terms extended ~30% in Q3. Newer framing tied to the AI transition. |

| AI-driven productivity and workforce reduction | emerged | Q2 2026, Q3 2026 | Coding agents, data-operations automation and a roughly 10% technology-workforce reduction are new levers management now cites as the path back to margin expansion. |

| Medium-term margin framework deferred | dropped | Q4 2025, Q1 2026 | The 37-38% medium-term adjusted-margin target from the November 2023 Investor Day has gone unreaffirmed; new leadership called medium-term guidance premature and points to an upcoming Investor Day for a refreshed plan. |

Guidance ledger

Quotes, calls, and speakers are source-verified; outcomes are curator-classified.

| Verbatim guidance | Call | Speaker | Curator outcome | Outcome note |

|---|---|---|---|---|

| “we are guiding to incremental organic ASV growth of $90 million to $140 million, reflecting a 5% growth rate at the midpoint of our range” | FactSet Research Systems Inc., Q4 2024 Earnings Call, Sep 19, 2024 · 2024-09-19T15:00:00 | Helen Shan | kept | FY2025 closed with $127 million of organic ASV added, described as near the top end of the range on the Q4 2025 call. |

| “adjusted EPS is expected to be in the range of $16.80 to $17.40.” | FactSet Research Systems Inc., Q4 2024 Earnings Call, Sep 19, 2024 · 2024-09-19T15:00:00 | Helen Shan | kept | FY2025 adjusted EPS came in at $16.98, within the guided range per the Q4 2025 call. |

| “we're guiding to organic ASV growth of $100 million to $150 million, representing approximately 5% growth at the midpoint” | FactSet Research Systems Inc., Q4 2025 Earnings Call, Sep 18, 2025 · 2025-09-18T13:00:00 | Helen Shan | pending | Initial FY2026 ASV range; subsequently raised to $130-$160 million in Q2 2026 and Q3 ASV growth of 7.1% is running above the midpoint. Fiscal year not yet complete. |

| “Our adjusted EPS guidance range is from $16.90 to $17.60.” | FactSet Research Systems Inc., Q4 2025 Earnings Call, Sep 18, 2025 · 2025-09-18T13:00:00 | Helen Shan | pending | Initial FY2026 adjusted EPS range; later raised to $17.25-$17.75 in Q2 2026. Full-year outcome not yet reported. |

| “ASV growth is now expected at $130 million to $160 million, representing approximately 5.4% to 6.7% growth” | FactSet Research Systems Inc., Q2 2026 Earnings Call, Mar 31, 2026 · 2026-03-31T13:00:00 | Helen Shan | pending | Raised FY2026 ASV range after a strong first half; Q3 organic ASV growth of 7.1% is at or above the top of this range, but the year is not yet closed. |

| “We remain confident in the guidance ranges that were previously set for ASV, revenue, operating margin and EPS. On revenue and EPS in particular, we are tracking toward the high end of those ranges” | FactSet Research Systems Inc., Q3 2026 Earnings Call, Jul 01, 2026 · 2026-07-01T13:00:00 | Joshua Warren | pending | Q3 2026 reaffirmation of the raised FY2026 ranges; final Q4 results not yet reported. |

Q&A pressure map

Question counts and firms are curator tallies; analyst coverage shown above.

| Topic | Questions | Firms | Pressure / response |

|---|---|---|---|

| Margin trajectory and investment economics | 4 | UBS, Morgan Stanley, Wells Fargo, BofA Securities | The most-pressed cluster on the latest call: the ~300 bp year-over-year margin decline, one-time costs rolling into FY2027, investment payback periods and token-cost drag. Management pointed to a line of sight on improvement but gave few hard numbers, a recurring point of tension across recent quarters. |

| AI monetization | 3 | Deutsche Bank, Autonomous Research, William Blair | Analysts repeatedly probed how AI adoption translates into revenue beyond ASV optics; management leaned on adoption metrics and upsell rather than a discrete pricing mechanism. |

| ASV guidance conservatism | 1 | RBC Capital Markets | Opening question challenged why guidance implies a Q4 slowdown despite strong momentum; management cited a record year-ago comparison and its practice of not changing guidance intra-year. A theme analysts have raised in prior quarters as well. |

Language shifts

Only language evidence verified against the referenced component is shown.

| Observation | Verbatim evidence | Call ID | Component |

|---|---|---|---|

| Management's framing has shifted to positioning FactSet itself as core AI infrastructure, a more assertive claim than the 'trusted data' language of prior calls. | “As AI reshapes financial institutions, FactSet is becoming mission-critical AI infrastructure.” | 2003511099 | 2 |

| A new cost-and-efficiency vocabulary around AI-driven headcount reduction appears, absent from earlier calls that emphasized adding headcount. | “we initiated a roughly 10% reduction in our technology workforce” | 2003511099 | 2 |

| Token cost is introduced as an entirely new expense category, explicitly flagged as not previously modeled. | “Tokens are an interesting one in the sense that they were not a line item that we really thought about in 2025. So all of the token spending is net new.” | 2003511099 | 43 |

| The caution vocabulary of the prior-year guidance ('conservative,' 'longer sales cycles') has given way to acceleration language, marking a confidence shift versus the Q4 2025 setup. | “We are taking a conservative approach to our guidance to reflect the current environment of longer sales cycles and more rigorous client approval processes” | 1958502923 | 3 |

The call history shows a company mid-transition — new CEO and CFO, accelerating ASV and an aggressive AI pivot — with the debate now centered on whether AI-driven productivity converts the current margin compression back into expansion. Management's confidence has visibly risen, but the guidance is still reaffirmed rather than chased higher, and the deferred medium-term margin framework leaves the Investor Day as the next real test.

What FactSet is, and why the price has halved

FactSet sells financial data, analytics and workflow software to the investment industry on multi-year subscriptions, and it has grown revenue for 45 consecutive years and diluted EPS for 29. Yet the shares have fallen from $495.72 in November 2024 to $262.46, roughly halving, as organic growth slowed to mid-single digits and the market began pricing generative AI as a threat to the terminal-and-data model. This chapter orients a cold reader and fixes the question the report exists to answer.

Share price (16 Jul 2026)

From Nov-2024 peak

Market cap ($B)

FY2025 revenue ($M)

Annual Subscription Value ($M)

FY2025 diluted EPS

Sources: price, market cap and drawdown computed from daily market prices (all-time-high close $495.72 on 14 Nov 2024; $262.46 on 16 Jul 2026); revenue and EPS from the FY2025 Form 10-K [1] [2]; ASV from the FY2025 10-K [3].

The business, in plain terms

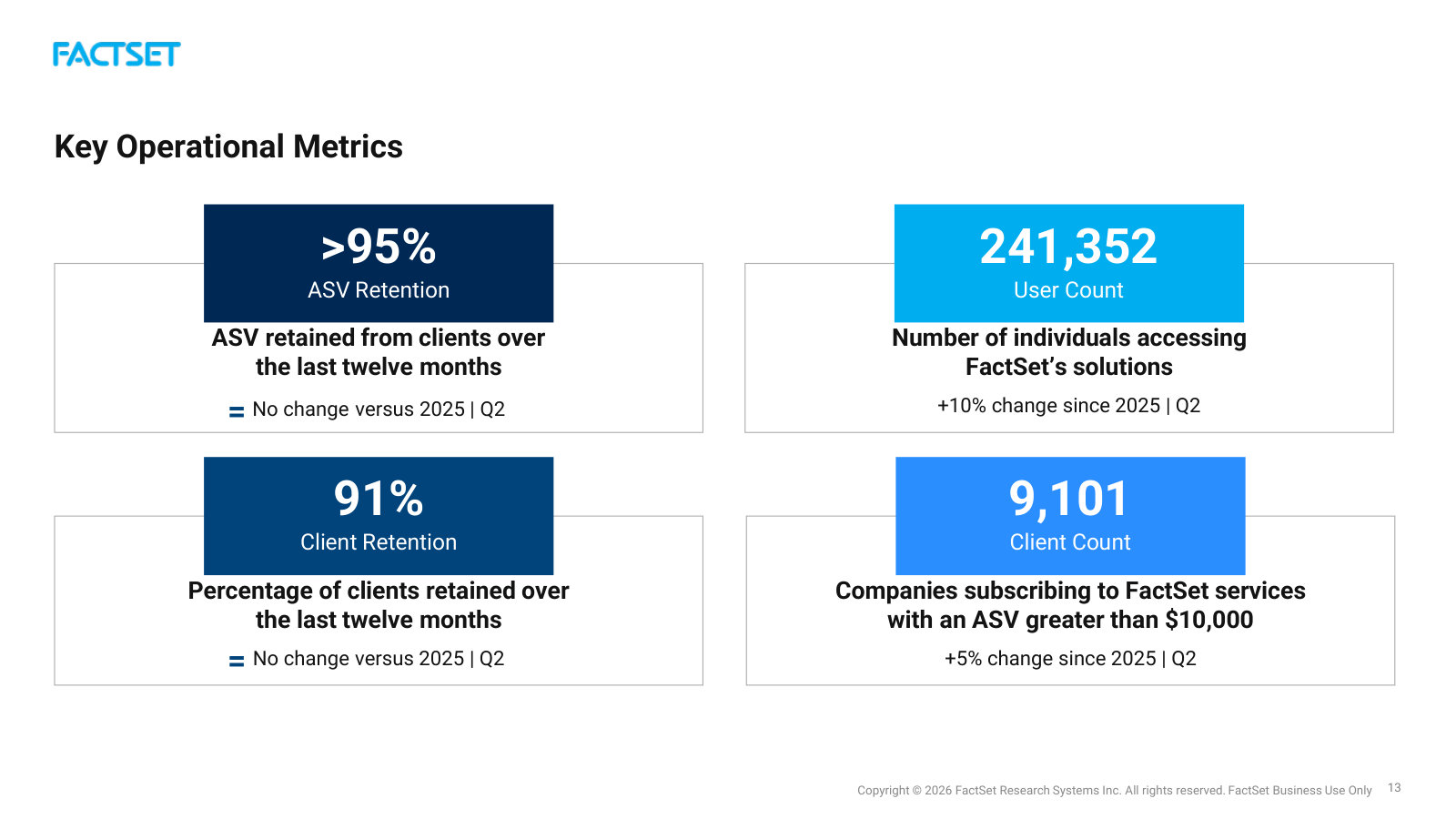

FactSet (Norwalk, Connecticut; founded 1978; fiscal year ends 31 August; NYSE: FDS) aggregates market, fundamental, and alternative data and delivers it through a workstation, feeds, and analytics that portfolio managers, sell-side bankers, wealth advisers, and corporate teams use to research, model, and monitor investments. Revenue is almost entirely recurring: clients contract for a defined set of data and users, and the sum of those annualized contracts is the company's headline operating metric, Annual Subscription Value (ASV), which stood at $2,405.6 million at the end of FY2025 [4].

The switching costs show up in the numbers a value investor cares about first. At FY2025 year-end FactSet served 8,996 clients and 237,324 users [5], retained more than 95% of ASV over the trailing year, and kept 91% of clients by count [6]. Its customer base is the industry's core: 95 of the top 100 global asset managers, 43 of the top 50 investment banks, and 37 of the top 40 wealth firms, with nine of its ten largest clients on the platform for more than 20 years [7].

That embeddedness is what has powered a rare compounding record: 45 consecutive years of revenue growth, 29 consecutive years of EPS growth, and 27 consecutive years of dividend increases [8]. Users have more than doubled since FY2018.

Source: user counts by fiscal year from FactSet segment KPI disclosures, consolidated into the FY2025 10-K figure of 237,324 [9].

The economics: high-margin, cash-generative, lightly levered

FactSet converts that recurring revenue into wide margins. FY2025 revenue was $2,321.7 million and operating income $748.3 million — a 32.2% operating margin, up from 25.8% in FY2022 [10] [11]. Diluted EPS rose 11.8% to $15.55, and the company returned $460.4 million to shareholders through buybacks and dividends during the year [12].

Source: consolidated statements of income, FactSet FY2023 10-K (FY2021–FY2023) [13] and FY2025 10-K (FY2024–FY2025) [14].

The balance sheet is conservative for a business that carries acquisition debt: about $1.37 billion of total debt against roughly $0.34 billion of cash and $726 million of operating cash flow in FY2025. Interest is covered many times over, and net leverage sits near one-and-a-half times cash earnings. For a reader who wants the probability of bankruptcy near zero, FactSet clears that bar comfortably — the debt was taken on to buy the CUSIP Global Services franchise, not to plug an operating hole, and it is amortizing.

Why the market marked it down

Two things changed at once. First, growth decelerated. Reported revenue growth fell from 15.9% in FY2022 to 5.4% in FY2025, and — stripping out the CUSIP acquisition that flattered FY2022–FY2023 — organic ASV growth was 4.8% in FY2024 and 5.7% in FY2025 [15] [16]. A franchise the market had valued as a mid-teens compounder was resetting to mid-single digits.

Source: year-over-year growth computed from consolidated revenue in the FY2023 and FY2025 10-Ks [17] [18].

Second, the story got harder to underwrite. Generative AI cuts both ways for a data vendor — it can lower the cost of assembling data and answering research questions, which threatens the premium a workstation commands, even as FactSet embeds the same tools in its own products. And in June 2025 the board replaced Phil Snow, a 30-year insider and CEO of a decade, with Sanoke Viswanathan, a 15-year JPMorgan executive and the first outsider to run the company in its modern history [19]. A first-time outside CEO arriving as growth slows is a governance change a buyer has to price.

The result is a sharp de-rating. At its November 2024 peak the stock traded near 35.6 times trailing earnings; at $262.46 it trades at 16.9 times FY2025 EPS and about 14.7 times the $17.81 the analyst consensus expects for FY2026 — a market multiple for a business that spent years commanding a large premium.

Source: calendar year-end closing prices from daily market data; the intraday-basis all-time-high close was $495.72 on 14 November 2024.

The through-line this report follows

FactSet is a fallen star: a best-in-class financial-data franchise, with 95%-plus ASV retention and a 45-year growth record, whose shares have roughly halved from their late-2024 peak as organic growth settled into the mid-single digits and the market began pricing generative AI as a structural threat to the data-and-terminal model. The question this report exists to answer is whether the de-rating has handed a value investor a genuine margin of safety — in a business whose bankruptcy risk is near zero — or whether roughly 15 times forward earnings still overpays for a franchise that no longer compounds the way its record implies.

Two facts frame that question honestly. In FactSet's favor: the moat is visible in the retention and client-tenure data, the cash conversion is high, and the balance sheet removes the tail risk this reader most fears. Against it: FactSet is not founder-run — insiders own little, and a first outside CEO is arriving precisely as growth slows — so the "skin in the game" this reader prizes is thin, and the AI question is genuinely unresolved. What would settle it is evidence over the next several quarters on whether organic ASV growth stabilizes or keeps sliding, and whether AI shows up as a tailwind in FactSet's own pricing or as a discount in its clients' willingness to pay. The chapters that follow test each leg in turn.

The Financial Record

FactSet's five-year record reads like a quality compounder: revenue up from $1.59 billion (FY2021) to $2.32 billion (FY2025), a near-27% free-cash-flow margin, and $460 million returned to owners in FY2025 alone. But the FY2025 headline flatters the trend. Reported diluted EPS rose 11.8%; on an adjusted basis, stripping a one-time divestiture gain and an easy prior-year comparison, it grew 3.2%. The cash generation is real and durable; the "double-digit growth" is not.

Five years of revenue and margin

Revenue compounded at roughly 9.8% a year from FY2021 to FY2025, but the shape of that growth changed. The FY2022–FY2023 mid-teens jump was lifted by the March 2022 acquisition of CUSIP Global Services (CGS); reported growth then settled to 5.6% in FY2024 and 5.4% in FY2025 as that acquisition annualized and organic demand did the work [1].

Source: FY2025 Annual Report (Form 10-K), Consolidated Statements of Operations [2]; earlier years from FY2022 Annual Report (Form 10-K) [3].

Reported operating margin tells a story that needs a footnote. It rose from 25.8% in FY2022 to 32.2% in FY2025 — a 640-basis-point expansion the bull case leans on. But FY2022 was a depressed base: FactSet took a $64.3 million asset-impairment charge that year (of which $62.2 million came from vacating leased office space as it resized its real-estate footprint for hybrid work), which alone cut roughly 350 basis points off the margin [4]. Measured from FY2021's 29.8%, the expansion to 32.2% is closer to 240 basis points over four years.

Source: derived from reported financials, FY2021–FY2025 10-Ks; FY2022 impairment detail per FY2022 Annual Report (Form 10-K) [5].

What the FY2025 headline leaves out

The gap between reported and underlying growth is the single most useful thing this record shows a new investor. FactSet's own non-GAAP reconciliation makes the point without editorializing: reported operating income grew 6.7% in FY2025, but adjusted operating income grew 1.3%, and adjusted operating margin actually fell, from 37.8% to 36.3% [6].

Reported diluted EPS rose 11.8% in FY2025. Adjusted diluted EPS rose 3.2%. The difference is a $0.45-per-share gain on a business divestiture in the current year and a weak prior-year base that carried a $1.03-per-share sales-tax charge.

The mechanics sit on the income statement. FY2025 pretax income grew faster than operating income because "other income (expense), net" swung from negative $49.8 million to negative $27.3 million — a $22.5 million improvement driven largely by a $22.4 million other-income line that houses the divestiture gain, plus lower interest expense as debt was paid down [7]. Management states plainly that the rise in net income and EPS was "primarily driven by higher operating income and a gain from the divestiture of a business" [8].

Source: FY2025 Annual Report (Form 10-K), non-GAAP reconciliation of operating income, net income and diluted EPS [9].

None of this is aggressive accounting — the adjustments are disclosed and the items are genuinely one-time, cutting both ways across years. The point is calibration: a reader who anchors on "EPS up 11.8%" will overstate how fast this franchise actually compounds. The underlying rate in FY2025 was low single digits.

Cash conversion is the durable part

Where the record holds up unambiguously is cash. Operating cash flow rose every year from FY2021 to FY2025, reaching $726 million, and free cash flow (after a rising capital-expenditure line) reached $617 million — a 26.6% free-cash-flow margin and roughly 1.0x conversion of net income [10]. The divestiture gain does not flatter this figure: the non-cash gain is removed in the cash-flow statement, and only the $25 million of cash proceeds sits in investing activities [11].

Source: FY2025 Annual Report (Form 10-K), Free Cash Flow table and Consolidated Statements of Cash Flows [12].

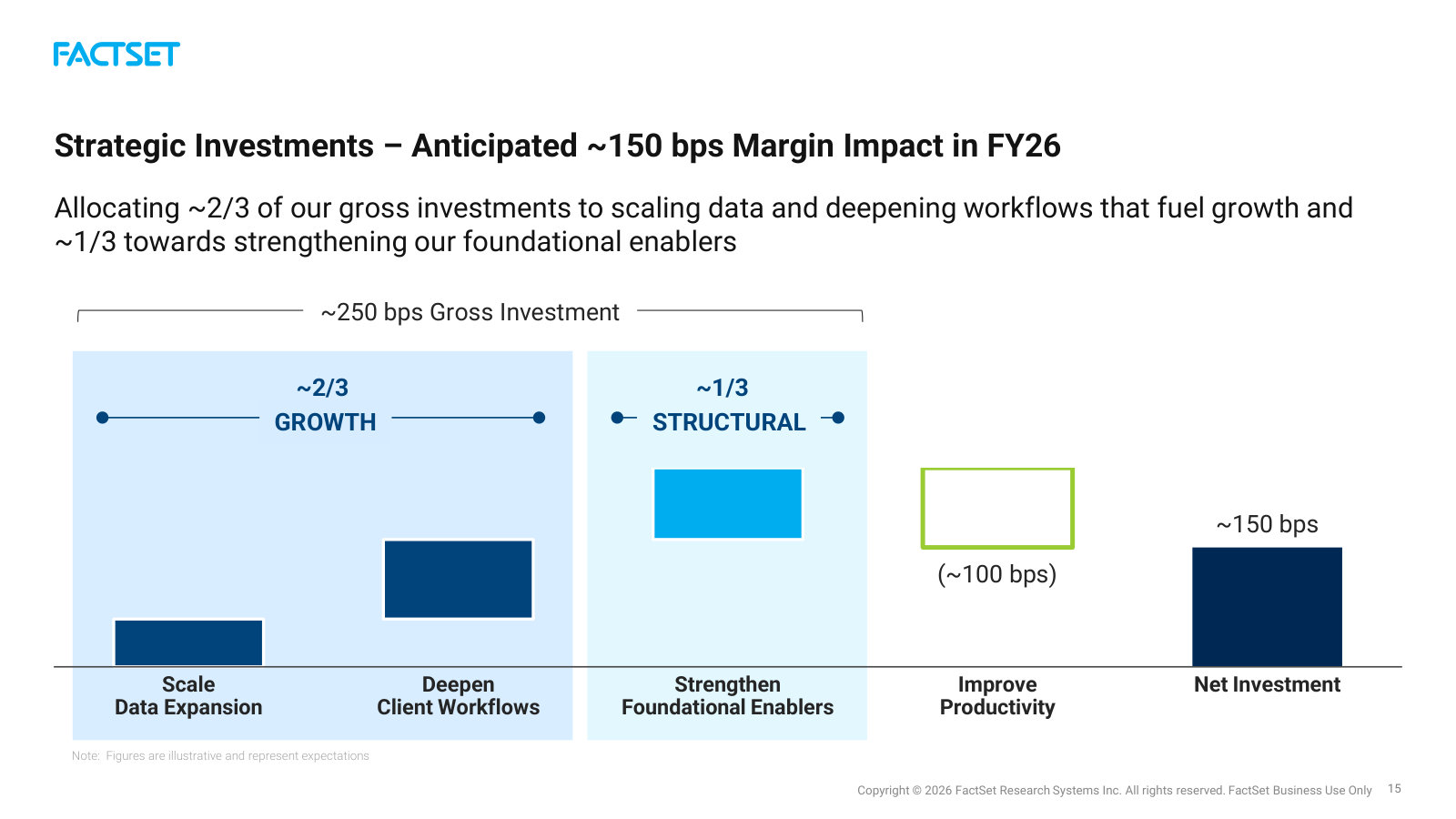

One watch item lives inside that cash line. Capital expenditure — property, equipment and capitalized internal-use software — climbed from $60.8 million in FY2023 to $85.7 million in FY2024 and $108.8 million in FY2025, which is why free cash flow was essentially flat year-over-year (up $2.8 million) despite $26 million more operating cash [13]. The rising spend tracks the company's AI-platform build; whether it converts to faster ASV growth or simply resets the capex baseline is the question it raises.

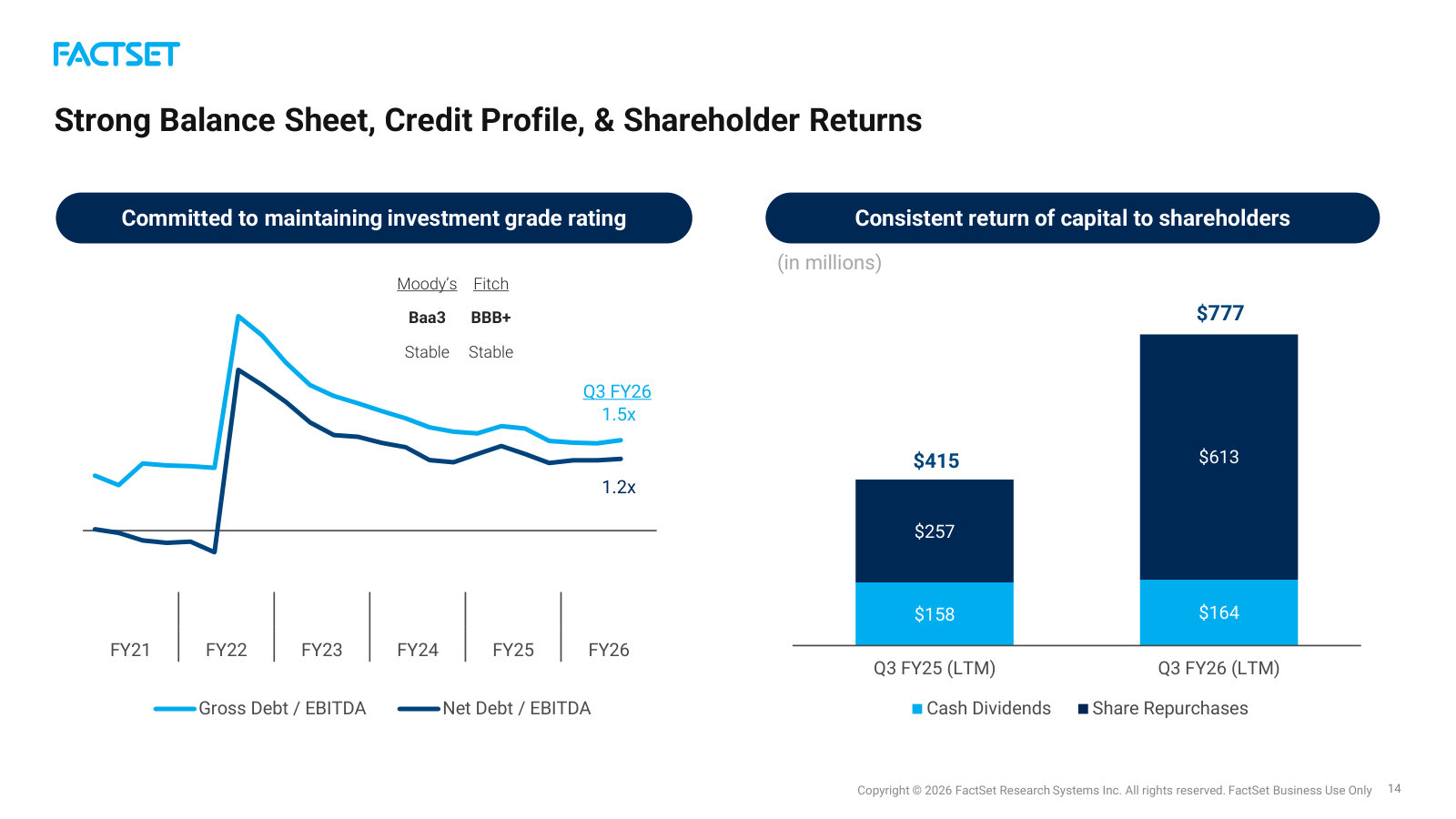

Capital returned, and a balance sheet with room

FactSet returned $460 million to shareholders in FY2025 — $160 million in dividends (a 27th consecutive year of increases) and $300 million in buybacks — against $617 million of free cash flow, a 75% payout that leaves headroom [14]. Notably, repurchases stepped up as the shares fell — $177 million (FY2023), $235 million (FY2024), $300 million (FY2025) — the pattern a value investor wants to see from management buying its own equity into a de-rating.

Source: FY2025 Annual Report (Form 10-K), Consolidated Statements of Cash Flows — financing activities [15].

The buybacks come with an asterisk. Diluted share count went from 38.6 million (FY2021) to 38.4 million (FY2025) — down only about 0.5% — despite roughly $1.0 billion of cumulative repurchases, because stock-based compensation and employee-plan issuance offset most of the retirement [16]. The repurchase program has largely defended the share count rather than shrunk it.

The balance sheet is the reader's insurance against the calibration mistake noted earlier. FactSet has deleveraged from the CGS-financed peak: net debt fell to about $1.03 billion and debt-to-equity to 0.63x (from 1.49x in FY2022), against $935 million of FY2025 EBITDA — roughly 1.1x net leverage [17]. During FY2025 the company refinanced, raising $803 million of new debt to repay $805 million of old [18]. Bankruptcy risk is not a live question here, which matters for a reader who has been burned by it before.

Where the growth actually comes from — and a recent inflection

Revenue is concentrated in the Americas, which produced 65% of FY2025 revenue; EMEA added 25% and Asia Pacific 10% [19]. Segment operating income by region is not a clean read of geographic profitability — FactSet centralizes most content and technology cost in the Americas, so the region carries the cost load while EMEA and Asia Pacific look far more profitable than they independently are — so the useful geographic signal is revenue, not segment margin.

Source: FY2025 Annual Report (Form 10-K), MD&A segment results by geography [20].

The forward-looking metric FactSet manages to is Annual Subscription Value — contracted forward revenue for the next twelve months. Organic ASV growth is where the recent record turns from a deceleration story into an inflection. It bottomed at 4.8% for FY2024 [21], recovered to 5.7% for FY2025 [22], and has climbed through FY2026 to 6.7% at February 2026 [23] and 7.1% at May 2026 [24]. The slowdown that framed the de-rating (De-Rated Compounder) is, on the most recent data, reversing.

Source: quarterly organic ASV growth as reported; anchor points per FY2025 10-K [25], Q2 FY2026 10-Q [26] and Q3 FY2026 10-Q [27].

What the forward estimates say

Consensus does not extrapolate the ASV re-acceleration into the earnings line. Sixteen-to-eighteen analysts model FY2026 revenue of about $2.47 billion (up 6.4%) and FY2027 of $2.61 billion (up 5.8%) — mid-single-digit top-line growth holding. On the bottom line, consensus adjusted EPS of $17.81 for FY2026 is only 4.9% above FY2025's adjusted $16.98 — consistent with the low-single-digit underlying rate this chapter identified, not the 11.8% GAAP headline.

Source: consensus analyst estimates (16–18 analysts), as of July 2026.

The sell side is unusually cautious for a franchise of this quality, which fits the "fallen star" frame. Of the most recent ratings, none were strong buys — two buys, ten holds, four sells and two strong sells — and the mean price target of $254 sits below the $262 spot price, with a $210-to-$340 range around it.

Price (16 Jul 2026)

Mean Target

Low Target

High Target

Source: consensus analyst price targets and recommendation distribution, as of July 2026.

The financial record, then, cuts two ways for the report's central question. The business is a genuine cash machine with a fortress balance sheet, disciplined-if-dilution-offsetting buybacks, and — most recently — re-accelerating subscription growth. Against that, its underlying earnings power grew low single digits in FY2025 once the divestiture gain and prior-year noise are removed, and the Street already prices modest growth with a mean target below the market. Whether that combination is a margin of safety or a fair price for a slower compounder is what the valuation work has to resolve.

Moat and AI

FactSet's advantage is measurable in one place above all: subscription retention. Annual ASV retention has held above 95% every year from FY2020 through FY2025, with client retention in a 90–92% band through a rate shock and a growth slowdown [1]. That durability, plus pricing power and deep workflow embedding, is a real moat — but a narrow one built on switching costs, not scale. Generative AI, the risk the de-rating priced, now reads on the evidence as more tailwind-at-the-margin than existential threat, with early but small monetization.

The moat is retention, not size

FactSet ended FY2025 with 8,996 clients and 237,324 users, retaining more than 95% of annual subscription value and roughly 91% of clients [2].

ASV Retention (min)

Client Retention

Clients

Users

Source: FactSet FY2025 Annual Report (Form 10-K), Item 1 Business — ASV retention stated as "greater than 95%" [3].

What makes the number a moat rather than a snapshot is that it barely moves. Across six fiscal years spanning the 2022 rate shock, the banking hiring slump, and the organic-growth trough covered in the Financial Record, client retention stayed within two percentage points of 91%, and ASV retention never fell below 95%.

Source: FactSet FY2021–FY2025 Annual Reports (Form 10-K), MD&A; ASV retention stated as "greater than 95%" in each year [4].

The mechanism behind the stickiness is embedding, not novelty. Management describes FactSet as running performance, attribution, and risk analytics for over 6 million institutional portfolios every night, and integrating more than 15 million wealth portfolios, used across clients' front, middle, and back offices [5]. Ripping that out means re-plumbing nightly production workflows, which is why the annual price increase has been a recurring driver of organic ASV in every 10-K — in FY2025, sales to existing clients and price increases lifted organic ASV 5.7% to $2,370.9 million [6]. By Q2 FY2026 management reported the annual Americas price increase contributed more than the prior year, attributing it to value, retention, and enterprise-agreement escalators [7].

The moat defends share; it does not confer scale

FactSet names its largest competitors as Bloomberg L.P., S&P's Market Intelligence division, and LSEG's Data and Analytics division (formerly Refinitiv), with BlackRock Aladdin, MSCI, and Morningstar as further competitive products [8]. Against that field, FactSet is small. Its $2.32 billion of FY2025 revenue is below Morningstar and MSCI, and a fraction of the diversified majors.

Sources: FactSet FY2025 10-K, competitor naming [9]; peer revenue per reported FY2025 annual results. Bloomberg is privately held and larger; LSEG's Data and Analytics division is also larger and is excluded from the bar because the indexed LSEG filing is a sub-entity.

Two cautions temper the chart. S&P Global and Moody's earn much of their revenue from credit ratings, not data workstations, so they are not clean comparables; the honest reading is that FactSet competes for the same data-and-analytics budgets as balance sheets several times its size, including Bloomberg's terminal franchise and LSEG's Refinitiv base. That gap is the strategic constraint behind the through-line: the moat has proven strong enough to defend share — retention above 95% — but not to out-grow a mid-single-digit market, which is why organic ASV growth sat in the 5–7% range even as retention held. Execution and breadth, not size, are what FactSet sells.

Generative AI: the threat the de-rating priced

The bear case is not speculative; it is written into the filings. FactSet first added a dedicated artificial-intelligence risk factor in its FY2023 10-K, warning that introducing generative AI could bring new liabilities [10]. By FY2025 the language had sharpened to name agentic AI and to concede directly that "third parties may be able to use AI to create technology that could reduce demand for our products and services," alongside a competition risk factor noting that many rivals "have significant AI capabilities and funding" [11].

Peer MSCI states the mechanism more bluntly than FactSet does: AI-enabled tools "may allow clients… to develop in-house capabilities to replace our products," and "large-scale data scraping and generative AI models trained on publicly available information could also diminish the perceived uniqueness and commercial value of our proprietary content" [12]. That is the disintermediation fear the market applied to FactSet when the multiple compressed. And FactSet's own early record fed the doubt: when it launched its GenAI assistant, FactSet Mercury, management said monetization "remains under discussion" and was "not included in this year's guidance" [13].

Generative AI: the tailwind now in the numbers

Two years on, monetization has moved from theory toward evidence, though the dollar base is still small. FactSet guided GenAI products to add only 30–50 basis points of ASV in FY2025, and its new CEO cautioned that firms "often underestimated the complexity involved in realizing" AI's value [14]. By Q3 FY2026 the tone had turned concrete: management said over 10% of the quarter's ASV growth came directly from AI SKUs, more than 20% of its top-100 clients were using its Model Context Protocol (MCP) data connectors on a paid basis, and one top-ten client "literally doubled their data subscriptions with us because of AI," and, on the moat, said the connected data and embedded workflows are "starting to see evidence rather than theory" [15]. Management added that MCP-linked deals improved contract value roughly 90% of the time [16].